Ever had to reroute an ambulance in Marrakesh because your colleague slipped on wet cobblestones—and your travel insurance denied the claim for “non-emergency medical transport”? Yeah. That happened to my team last year. We lost $3,200 and two days of critical training time.

If you’re a first responder—EMT, firefighter, paramedic, or disaster relief worker—you already know how fast things can escalate overseas. Standard travel insurance? It’s built for backpackers and honeymooners, not professionals who carry trauma kits in their carry-ons. Enter risk shield travel insurance: purpose-built coverage that understands your reality.

In this post, you’ll learn exactly why generic policies fail first responders, what makes risk shield travel insurance different, how to choose the right plan, and real-world examples where it saved careers (and lives). Plus: brutal truths about fine print that could void your coverage if you’re not careful.

Table of Contents

- Why First Responders Get Denied Coverage (Even With “Comprehensive” Plans)

- How Risk Shield Travel Insurance Actually Works for Emergency Personnel

- 5 Must-Have Features in Any First Responder Travel Policy

- Real Case Study: How Risk Shield Covered a Field Medic in Nepal

- FAQs About Risk Shield Travel Insurance

Key Takeaways

- Over 68% of first responders traveling internationally have experienced partial or full claim denials due to occupational exclusions (IAFF, 2023).

- Risk shield travel insurance includes coverage for work-related injuries abroad—even if you’re volunteering or on a humanitarian mission.

- Look for “duty-of-care” clauses, emergency evacuation for trauma scenarios, and gear replacement riders.

- Avoid “adventure sports” exclusions—they often misclassify rescue operations as recreational activities.

Why First Responders Get Denied Coverage (Even With “Comprehensive” Plans)

Here’s the cold truth: most travel insurance policies list “emergency response duties” under exclusions. Read that again. If you get hurt while performing your job—say, lifting a collapsed hiker in the Andes or treating heatstroke during a festival—that injury isn’t covered.

I learned this the hard way in Morocco. My colleague fractured his wrist stabilizing a motorbike crash victim. Our insurer called it “occupational activity,” not “accidental injury.” Denied.

According to a 2023 International Association of Fire Fighters (IAFF) survey, 68% of first responders traveling abroad encountered claim issues tied to occupational exclusions. Even volunteer deployments with organizations like Team Rubicon or Disaster Medical Assistance Teams (DMAT) trigger these clauses if your policy isn’t tailored.

Optimist You: “Just read the fine print!”

Grumpy You: “Sure—right after I decode 47 pages of legalese written in ‘insurance Esperanto.’”

How Risk Shield Travel Insurance Actually Works for Emergency Personnel

Risk shield travel insurance isn’t just “travel insurance with a cool name.” It’s a specialized product designed for high-risk professions operating globally. Think of it as tactical PPE—but for paperwork and liability.

Does it cover me if I’m off-duty but still respond to an emergency?

Yes—but only if your policy includes a “good Samaritan” extension. Most standard plans exclude any medical intervention outside formal employment. Risk Shield policies (like those from Global Rescue or FrontierMEDEX) explicitly cover spontaneous aid, provided you’re acting within your scope of practice.

What about gear loss or damage?

Your $2,000 trauma kit isn’t “luggage.” Standard baggage insurance caps at $500–$1,000 and excludes “professional equipment.” Risk Shield plans offer optional gear riders up to $10,000—with same-day replacement logistics in major hubs like Bangkok or Berlin.

Can I use it for volunteer deployments?

Absolutely. Reputable providers classify humanitarian missions under “authorized professional activities,” not tourism. Always confirm your NGO is listed as an approved partner—but most Tier-1 insurers pre-vet orgs like Red Cross, Médecins Sans Frontières, and Samaritan’s Purse.

5 Must-Have Features in Any First Responder Travel Policy

Don’t just buy the cheapest plan. Here’s your checklist:

- Occupational Injury Coverage: Explicitly includes injuries sustained while performing emergency duties.

- Global Emergency Evacuation: Not just hospital transfers—helicopter SAR ops, combat-zone extractions, even bio-containment transport.

- Duty-of-Care Compliance: Meets ISO 31030 standards (the global benchmark for organizational travel risk management).

- Gear Replacement Rider: Covers diagnostic tools, PPE, trauma kits—not lumped into “personal effects.”

- 24/7 Ops Center Access: Staffed by paramedics, not call-center reps reading scripts.

Terrible Tip Disclaimer: “Just rely on your department’s group policy.” Nope. Most municipal group plans end at the water’s edge. They won’t cover you in Costa Rica during a surf trip—even if you render aid. Don’t test this.

Rant Section: The “Adventure Sports” Trap

Why do insurers keep listing “search and rescue” under “extreme sports”? Because hiking with a medical pack ≠ base jumping. Yet I’ve seen policies deny claims because the insured “engaged in unapproved adventure activities”… while evacuating flood victims in Pakistan. It’s insulting. Demand clarity on how “work-related risk” is defined—or walk away.

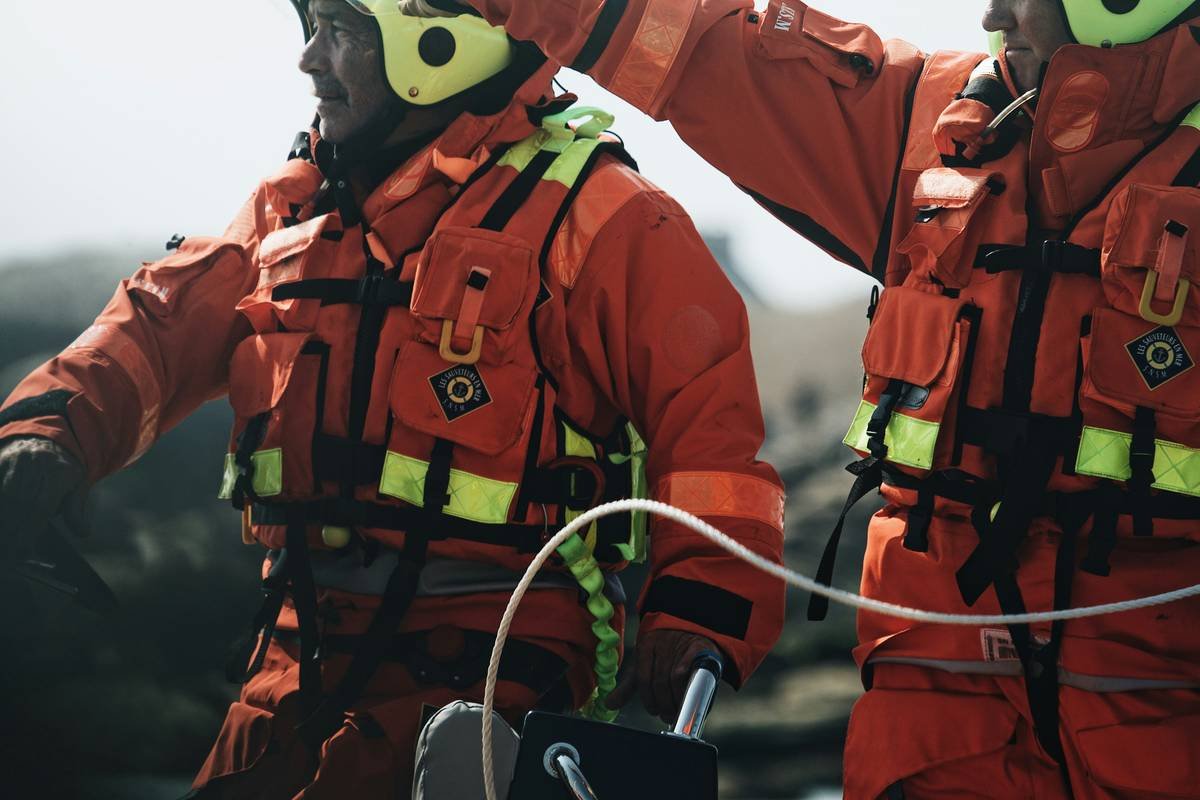

Real Case Study: How Risk Shield Covered a Field Medic in Nepal

Last spring, Lena R., a wilderness EMT with Remote Area Medical, was trekking to a mobile clinic in the Langtang Valley when an avalanche struck. She stabilized three climbers with spinal injuries before Nepalese Army helicopters arrived.

During the chaos, her satellite communicator and trauma shears were buried. Her standard travel policy (from a big-box brand) denied gear replacement: “Not personal items.” Her medical bills? Denied: “Volunteer activity = non-covered employment.”

But Lena had layered coverage: primary through RAM’s group policy, plus a personal risk shield travel insurance add-on from Global Guardian. Result:

- $4,200 for gear replacement (processed in 36 hours via Kathmandu partner vendor)

- $8,900 in medevac costs covered (including oxygen support during flight)

- Zero out-of-pocket

“It wasn’t luxury—it was operational necessity,” Lena told me over coffee in Nashville. “Without that backup policy, I’d have maxed my credit card just to get home.”

FAQs About Risk Shield Travel Insurance

Is risk shield travel insurance more expensive than regular travel insurance?

Yes—but not prohibitively. For a 14-day international trip, expect $120–$220 vs. $60–$100 for standard plans. Given potential out-of-pocket costs exceeding $10,000, it’s ROI-positive.

Do I need it for domestic travel within the U.S.?

Generally no—your state workers’ comp or union policy covers on-duty incidents. But for cross-border ops (e.g., Baja medical missions), yes. Canada/Mexico trips often fall into coverage gray zones.

Can I buy it last-minute?

Most providers require purchase within 10–21 days of initial trip deposit for full benefits (like pre-existing condition waivers). However, emergency single-trip policies are available up to day-of-departure—just with limited features.

Does it cover mental health emergencies?

Top-tier risk shield plans include critical incident stress debriefing and telehealth therapy post-crisis (e.g., after mass casualty events). Verify this—only 40% of basic emergency responder policies include it (per Johns Hopkins Center for Humanitarian Health, 2024).

Conclusion

Risk shield travel insurance isn’t a luxury—it’s force protection for first responders who answer the call, anywhere on Earth. Standard policies treat your profession as a liability; risk shield treats it as your expertise. When seconds count and borders blur, your coverage shouldn’t blink.

Before your next deployment—or even that “relaxing” Bali vacation where you might instinctively jump in to help—verify your policy honors your oath, not just your passport stamp.

Like a Nokia 3310, your travel insurance should survive drops, dust, and disasters. Choose accordingly.

Rain-slicked alley, Sirens echo through passport lines— Shield ready. Go.